What is Opportunity Cost?

Opportunity cost can be defined as the potential benefit that an individual misses out on by choosing one option over another. When an individual prefers one alternative over another, then the non-absorbed profit of the latter alternative is the opportunity cost. Opportunity cost generally remains overlooked and creates a barrier for businesses to make informed decisions. By considering the opportunity cost of different options, individuals and organisations can make decisions that can maximise their utility or benefit. Opportunity Cost theory is given by Gottfried Haberler and opportunity cost is also called alternative cost. Opportunity cost example is choosing to prepare for an exam instead of hanging out with friends has an opportunity cost in terms of the enjoyment and social contact you will lose.

Geeky Takeaways:

- The concept of opportunity cost is based on the principle that resources are limited.

- Every decision to choose a product over another has an opportunity cost associated with it.

- Opportunity cost helps to determine the most efficient allocation of resources.

Table of Content

- How Does Opportunity Cost Work?

- How Does Opportunity Cost Affect Decision Making?

- How Opportunity Cost is Calculated?

- Types of Opportunity Cost

- Law of Opportunity Cost

- Critical Evaluation of Opportunity Cost

How Does Opportunity Cost Work?

Opportunity cost is defined as the loss of benefit that arises due to choosing one option over another. For example, if you decide to study for an exam instead of going to a movie, the opportunity cost is the enjoyment and entertainment you could have had at the movie. By considering the opportunity cost of different options, individuals and organisations can make decisions that can maximise their utility or benefit. Opportunity cost can also be thought of as a trade-off. When one makes a decision, he/she is trading one option for another. Understanding the opportunity cost of different options can help in making informed decisions that align with the values and goals.

How Does Opportunity Cost Affect Decision Making?

Opportunity cost is an important concept to consider during the decision-making process as it helps individuals and organisations compare the costs and benefits of different alternatives and choose the best one among them. In the determination of various financial aspects too, (such as capital budgeting, cost accounting, etc.) evaluation of the opportunity cost of different investment proposals helps a business in determining which projects maximise the returns and minimise costs and risks.

How Opportunity Cost is Calculated?

The formula for the calculation of opportunity cost involves the difference between the expected returns of both alternatives; the one that an individual chose and the other that he/she didn’t choose.

Formula of Opportunity Cost:

Opportunity Cost = Return from Best-forgone Options – Return from Chosen Option

Opportunity Cost Example:

Let assume you have ₹10,000 to invest and their are two options available:

| Option A | Option B |

|---|---|

| Investing in a fund with an expected ROI of 8%. | Investing in a fund with a guaranteed ROI of 4%. |

You decide to choose Option B – Fund, for its guaranteed return and lower risk.

ROI on Option A – ₹10,000 x 8% = ₹800 per year – (Return from Best-forgone Options)

ROI on Option B – ₹10,000 x 4% = ₹400 per year – (Return from Chosen Option)

Opportunity Cost = Return from Best-forgone Options – Return from Chosen Option

Opportunity Cost = ₹800 – ₹400 = ₹400

By choosing the Option B – Fund, you give up the potential to earn an additional ₹400 annually that you could have earned from the Option A – Fund. This ₹400 represents your opportunity cost, the cost of choosing one option over another.

Types of Opportunity Cost

1. Implicit Cost: Implicit opportunity costs are the costs of using firms’ internal resources that can be used for other better purposes. Human Labour, Premises; etc., are some of the internal resources. Implicit opportunity costs are often overlooked because they are not directly visible. However, they can still have a significant impact on the overall cost of a decision. Implicit costs have already occurred in the business without any exchange of value, like employees.

Geeky Takeaways:

- Implicit costs are also known as Implied Costs and Imputed Costs.

- Implicit costs do not involve an exchange of cash or physical transfer of resources and, thus are not so easy to identify. But they have already been incurred in the business.

- Implicit costs are not recorded in the accounting process and generally remain invisible when it comes to making decisions between two alternatives.

2. Explicit Cost: Explicit opportunity cost refers to the opportunity cost that is explicitly stated or considered in a decision. Acquiring land, machinery, plants; etc., are examples of explicit costs. Explicit costs involve the transfer of cash or physical transfer of resources, thus they almost never remain overlooked while making decisions about what to choose among different alternatives.

Geeky Takeaways:

- Explicit opportunity costs are easy to identify because they are directly stated or visible.

- Explicit costs involve an exchange of cash or a physical transfer of resources. These are thus known as Out of the Pocket Expenses of a firm.

However, Sunk costs, Managerial costs, and Adjustment Costs are not included during the calculation of opportunity costs. Sunk Costs are the costs that have been incurred in the past and can never be recovered, like, advertisement expenses. Managerial Costs are the costs that arise due to the introduction of some new product in the business. Adjustment Costs are the costs that the company needs to bear in order to change the production process in response to market demand.

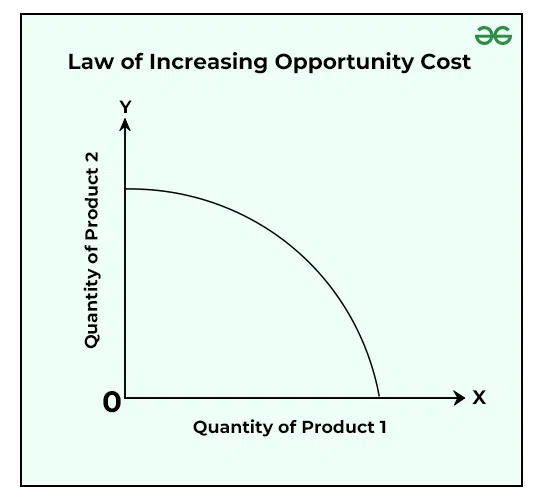

Law of Opportunity Cost

Opportunity cost diagrams can be prepared on the basis of increasing, decreasing and constant law of opportunity cost. Here is the Graphical Representation of Opportunity Cost Curve.

1. Law of Increasing Opportunity Cost:

The Law of Increasing Opportunity Cost states that as the production of a firm rises, opportunity cost tends to rise. When the production of one product increases, the production of other product tend to decline and the loss of benefit of the latter product is termed as opportunity cost. Allocation of resources tends to shift from one product to another. In the Law of Increasing Opportunity Cost, it is said that the company was better off using the resources for the intended purpose.

2. Law of Decreasing Opportunity Cost:

The Law of Decreasing Opportunity Cost states that a firm’s opportunity cost tends to decline when it decides to allocate its resources from one product to another. When the cost of producing one unit decreases, the cost of production of the next unit will also decline. In this scenario, production cost tends to decline as the production rises, thus declining the opportunity cost.

3. Law of Constant Opportunity Cost:

The Law of Constant Opportunity Cost refers to a situation in which the costs associated with pursuing a certain opportunity remain constant but the advantages of doing so change. The phrase is widely used to describe a manufacturing technique that allows for increasing output while maintaining the same cost of production for goods and services.

Critical Evaluation of Opportunity Cost

Benefits of Opportunity Cost

1. Evaluation of different Alternatives: Opportunity costs highlight the loss of benefit that an individual/a company bears when they decide to choose one alternative over another.

2. Comparison of Prices: Opportunity costs help in comparing prices of different alternatives along with their respective risks and returns. Comparison of the total value of benefits derived from different alternatives is the main motive of this concept.

Limitations of Opportunity Cost

1. Subjective Approach: Opportunity cost of a particular choice may vary depending on an individual’s preferences, values, and circumstances. What one person considers to be a high opportunity cost may not be the same for another person. Thus, the concept of opportunity cost is subjective in nature.

2. Considers only Explicit Costs: Opportunity costs only take into account the explicit costs of a decision. It does not consider implicit costs.

3. Does not Consider Time Value of Money: Opportunity cost does not take into account the fact that the value of money changes over time due to inflation. This means that the opportunity cost of a decision made today may be different from the opportunity cost of the same decision made in the future.

Leave a Reply